PeopleImages | E+ | Getty Images

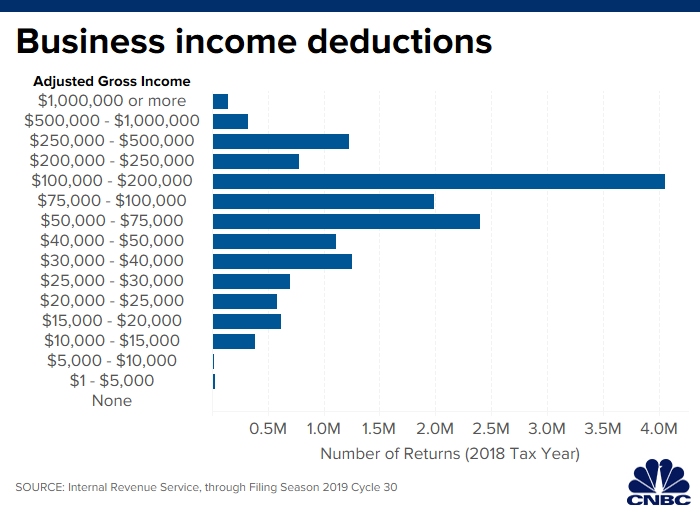

A tantalizing 20% tax break for business owners went into effect in 2018 — and more than 15 million taxpayers grabbed it.

The qualified business income deduction is one of the new features of the Tax Cuts and Jobs Act.

This new tax break allows owners of "pass-through" entities, including S-corporations, partnerships and sole proprietorships, to deduct up to 20% of their qualified business income.

About 11% of taxpayers claimed the deduction on their 2018 returns as of July 25, according to data from the Internal Revenue Service.

Up to that date, the IRS received more than 141 million returns.

More late filers will likely claim the deduction as accountants prepare for the Oct. 15 extension deadline.

Tax professionals are also digesting a new regulation from the IRS, just issued in September — a safe harbor that spells out the terms under which rental real estate can qualify as a business for the deduction.

"With it being the first year, I think everyone is still trying to figure it out," said Tim Steffen, CPA and director of advanced planning at Robert W. Baird & Co. in Milwaukee.

"You'll see that number go up as returns start coming in this fall," he said.

Are you eligible?

MoMo Productions | Taxi | Getty Images

As tempting as the deduction sounds, figuring out if you qualify is no easy feat.

Here's a breakdown of who can take it.

First, business owners in any industry may take the 20% deduction if they have taxable income that's under $157,500 if single or $315,000 if married and filing jointly in 2018.

The IRS applies limitations over those thresholds.

For starters, taxpayers in a "specified service trade or business," including doctors, lawyers and accountants, can't take the deduction at all if their taxable income exceeds $207,500 if single or $415,000 if married.

The rules are a little different for business owners who aren't in a "specified service trade or business."

In that case, you get a reduced deduction if your taxable income exceeds the $157,500/$315,000 threshold but is still under the $207,500/$415,000 threshold.

If your business isn't in a specified service trade or business, and your taxable income exceeds the $207,500/$415,000 threshold, then your deduction is generally capped as a percentage of W-2 wages paid to your employees.

Here's another consideration: The QBI deduction is only around until the end of 2025.

Breaks for landlords

ablokhin | Getty Images

In January 2019, the IRS proposed additional guidance for rental real estate owners, a safe harbor they can follow in order to be certain they qualify for the 20 percent deduction.

The agency finalized the safe harbor in late September, just weeks before the Oct. 15 deadline for 2018 filers on extension.

Those guidelines include maintaining separate books and records for each rental enterprise, as well as performing and documenting at least 250 hours of rental services in a year if the enterprise has been around for less than four years.

Landlords who've had their rental enterprise for longer than that must document at least 250 hours of rental services in three of the last five years.

Rental services include maintenance and repairs on the property and supervising people who work there.

Other tasks, including time spent purchasing property or traveling to and from your real estate, won't count toward the hourly requirement.

Even with the safe harbor, landlords will need to keep immaculate records to prove they're following the rules.

"Save your documents and receipts; you need to support your hours," said Troy Lewis, CPA, associate teaching professor at Brigham Young University and chairman of the qualified business income task force at the American Institute of CPAs.

Failure to meet the safe harbor doesn't mean you can't claim the deduction, but it does mean the burden of proof is on you if you're audited.

How to proceed

Thomas Barwich | Getty Images

As tempting as the 20 percent deduction is for small businesses, entrepreneurs should proceed with caution. Here's where to begin:

Keep well-documented books and records. Be sure to closely review the receipts and statements that pertain to your business, and prepare to turn these in to your accountant.

If you're hoping to claim the deduction for a property you rent out and do so under the safe harbor, the IRS will want to know how much time you spent on maintenance, management and more.

Think before making dramatic changes to your business. Last summer, the IRS put the kibosh on aggressive strategies accountants pitched to help entrepreneurs qualify for the break.

The qualified business income deduction is still a work in progress — and it's only around until the end of 2025 — so slow down before doing anything too drastic.

"The well-advised client will view this as another data point to reevaluate their structure and business," said Jonah Gruda, CPA and partner at Mazars USA. "But I always tell them that while tax is an important aspect of business decisions, it's only an aspect."

Talk to your accountant. Do a gut check of your appetite for the deduction, and prepare for the possibility that you may have to make your case to the IRS.

"There are gray areas where it's a matter of your tax risk tolerance," said Jeffrey Levine, CPA and CEO of Blueprint Wealth Alliance. "Are you a fighter, or are you going to say, 'I have bigger things to worry about'?

"I have clients in both camps," he said.

0 Comments